E-invoicing software UAE

What is e-invoicing software? Electronic invoicing (e-invoicing) software is a digital solution that enables businesses…

The UAE’s Corporate Tax Law (Federal Decree Law No. 47 of 2022) establishes a legislative framework for the introduction and implementation of federal corporate tax. Under the law, corporate tax in the UAE is a direct tax levied on the net income or profit of corporations and other entities from their business.

To understand corporate tax and its implications to your business, bear in mind first the upcoming deadlines for 2026 filing.

General rule is that corporate tax returns must be filed within 9 months after the end of your financial year (FY).

To ensure a smooth filing system, here are some updated guidelines for you and your business, including the updated amendments under Cabinet Decision 129 of 2025 (effective 14 April 2026) revising the UAE administrative penalty framework.

The UAE has introduced a federal corporate tax system effective from 1 June 2023. The standard corporate tax rate in the UAE is 9%, which is the lowest in the GCC region, except for Bahrain. The UAE corporate tax regime is designed to incorporate global best practices and minimize the compliance burden on businesses.

Tax applies to income earned from UAE operations, assets, or services for foreign entities with a permanent establishment in the UAE. Generally, all Taxable persons are subject to taxable income and payable to the Federal Tax Authority (FTA)

Note

Natural persons conducting business activities in the UAE are taxable if their annual turnover exceeds AED 1 million.

This applies to sole proprietors, freelancers and generally individuals holding a professional license or licensed to carry out commercial and service activities.

|

Terminology |

Definition |

|---|---|

|

Juridical Persons |

A legal entity created by law, separate from its owners or shareholders Automatically a taxable person under the law |

|

Natural Persons |

Refers to an individual human being and may be subject to corporate tax if they meet the annual turnover exceeding AED 1 million |

|

Taxable Income |

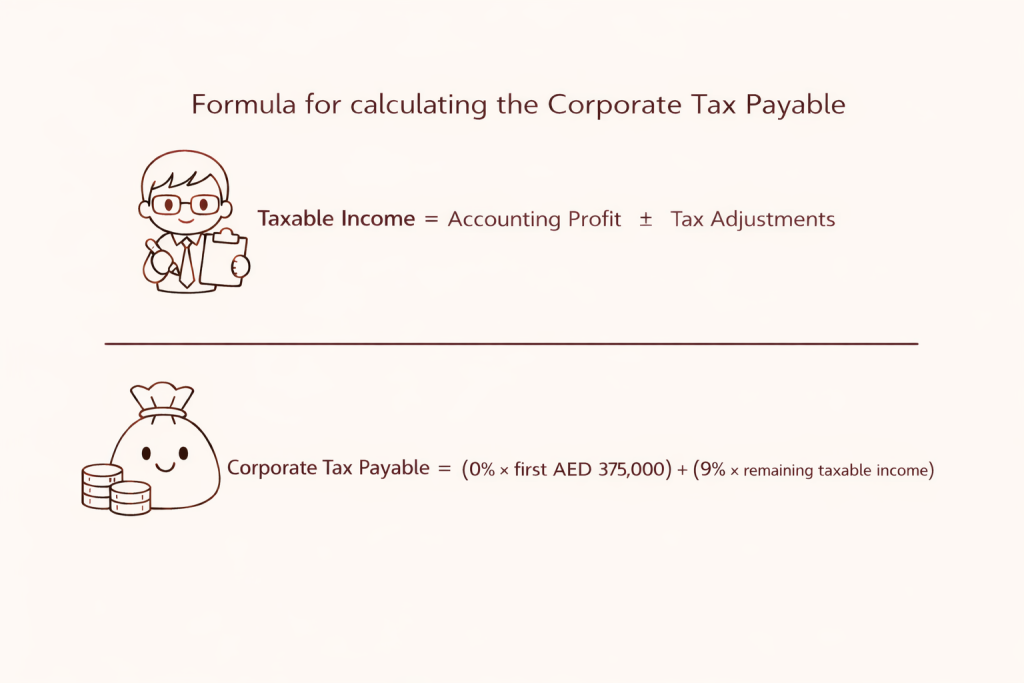

Income subject to CT under the Law. You arrive at the number by taking the accounting profit + tax adjustments Taxable income is what would be multiplied to the tax bracket it falls under |

|

Tax Returns |

Information filed with the Federal Tax Authority every end of a taxable period to maintain compliance and records of the tax payable (or in some cases, applicable tax relief) with the government |

|

Relevant Tax Period |

Period for which a tax return must be filed |

The UAE has adopted a dual-tier corporate tax system effective June 1, 2023, with a 0% tax rate on taxable income up to AED 375,000 and a 9% rate on income exceeding that amount.

Bear in mind that corporate tax is a direct tax applied per tax period.

The tax payable is calculated based on the taxable income and not the accounting profit. Taxable income is determined by applying adjustments starting from accounting income, then applying the correct tax rate based on the threshold.

In some cases, it is possible to have taxable income and still end up with little to no tax payable to the government.

There are a few exceptions, especially for:

Free Zone entities must comply with regulations to benefit from the 0% rate on qualifying income.

Small businesses with revenue up to AED 3 million can elect for Small Business Relief, allowing them to treat their taxable income as zero until the end of 2026 (Read our guide here).

The Domestic Minimum Top-up Tax (DMTT) has been implemented in the UAE starting January 1, 2025. The implementation of the DMTT is part of the UAE’s efforts to align with international tax transparency standards and prevent harmful tax practices.

The DMTT specifically targets MNEs with consolidated global revenues of €750 million or more in at least two of the four fiscal years preceding the tax year.

The DMTT ensures that large multinational enterprises (MNEs) pay a minimum effective tax rate of 15% on global profits.

A MNE Group is also defined as:

The UAE’s DMTT aligns with the OECD’s Two-Pillar Solution framework.

Table Summary of Corporate Tax Rates

|

Category |

Rate |

Threshold / Condition |

|---|---|---|

|

Standard taxable person |

0% |

up to AED 375,000 |

|

Qualifying Free Zone Person (QFZP) / qualifying income |

0% |

Applicable to qualifying income and if Free Zone entity meets conditions for granting of status |

|

QFZP / non-qualifying income |

9% |

Must meet De Minimis Threshold to retain QFZP status (a limit set by a Ministerial Decision on non qualifying revenue that a QFZP can earn): A QFZP must ensure that non qualifying revenue in a tax period:

|

|

Multi national enterprise groups (MNE) |

15% |

Consolidated global revenues of €750 million or more in at least two of the four financial periods preceding the tax year. |

A corporate tax return is essentially information filed with the Federal Tax Authority for CT purposes. It must be submitted in the form and manner prescribed by the FTA and covers one taxation period.

|

Component Type |

Details and Examples of Info Needed |

|---|---|

|

Taxable Person Details |

Typically these details are already available in your EmaraTax account after CT registration, but it helps to keep it updated as soon as changes happen to prevent any mistakes before filing your tax return. |

|

Current Taxable Period |

Every tax return corresponds to one specific taxation period. You cannot combine multiple periods in one return. For example:

|

|

Tax Elections (if applicable) |

The return includes elections such as:

|

|

Accounting or Financial Records |

|

|

Adjustments to determine income subject to CT |

Adjustments include:

|

|

Relief and Tax Losses |

|

|

Tax Liability and Tax Credits |

|

|

Review and Declaration |

|

To meet the strategic objectives of the federal government, all taxable persons must register for corporate tax with the Federal Tax Authority (FTA). The Ministry of Finance governs the Federal Tax Decrees, Cabinet Decisions, Ministerial Decisions and other implementing guidance under its authority, while Federal Tax Authority administers tax obligations.

Unlike traditional income tax systems applied to some jurisdictions, the UAE’s government bodies do not impose a broad personal income tax. Instead, they apply income tax direct towards businesses and certain natural persons conducting business in the UAE.

Understanding whether an entity is classified as Resident Person, a Nonresident Person, part of a Tax Group or an Person Exempt under UAE CT Law is essential in determining in determining filing obligations.

The corporate tax regime in the UAE applies to both resident and non-resident persons engaged in business activities within the country.

For resident juridical persons, the Corporate Tax base generally includes income derived from the UAE and from outside the UAE, subject to the exemptions and reliefs available under the law.

For natural persons – if they are eligible and meet the requirements for CT, bear in mind that only their business activities will be subject to corporate income tax. If an individual earns income in personal capacity, then corporate income tax may not apply.

For example, any capital gains on personal investments, other income and earnings that fall outside of their business activities are considered as exempt income.

The Corporate Tax Law also recognizes State-Sourced Income, but merely earning UAE-sourced income does not by itself necessarily require a foreign entity to register and file a normal UAE Corporate Tax Return.

For example, foreign banks would be subject to CT if they follow the conditions.

Separately, the law provides for withholding tax at a 0% rate on relevant State-Sourced Income categories unless a different rate is specified.

Because the filing and registration analysis for non-residents depends heavily on the precise fact pattern, businesses should avoid treating “UAE-sourced income” as an automatic filing trigger.

A tax group consists of two or more Taxable Persons treated as a single Taxable entity, subject to conditions. As a result, the parent company serves as the representative and files a single tax return.

A Qualifying Group allows certain reliefs while entities remain separate taxpayers. Transfers within a Qualifying Group may occur at net book value under prescribed conditions.

Tax loss transfers may be permitted between qualifying entities subject to conditions.

Intra group transactions between members of the same tax group are generally ignored for tax purposes, considering that they are treated as one taxable person. For example, if company A charges company B for management services, there is no impact on taxation at group level because both sit within the same group.

However, bear in mind that transfer pricing remains relevant for dealings with Related Parties and Connected Persons outside the Tax Group, and businesses should not assume that grouping removes all related-party compliance considerations.

We outline the specifics of tax group registration and its benefits and limitations in this free manual.

Certain types of businesses or organizations are exempt from Corporate Tax in the UAE due to their importance and contribution to the economy.

This participation exemption hinges on carrying out their activities as mandated in the license. If they deviate, the Federal Tax Authority may request certain exempt persons to register for corporate tax.

To know more about the nature of corporate taxation and applicable exempted entities, read here.

Businesses liable for corporate tax in the UAE must register with the Federal Tax Authority (FTA) and file returns within 9 months of the fiscal year-end.

All businesses registered for corporate income tax must submit, regardless if they have taxes owed to the government.

If they do have tax payable, it must be settled within the same deadline applicable to filing the tax returns.

The UAE corporate tax law allows businesses to carry forward tax losses to offset against future taxable income.

A tax loss also arises where a Taxable Person has negative taxable income for a tax period. This does not eliminate filing obligations. Tax loss may affect future income taxable computation for financial years beginning on or after 1 June 2023 under the CT framework.

The FTA’s tax returns guide also includes dedicated Tax Loss schedules where Taxable Persons must:

Note

When Small Business Relief (SBR) is applied, tax losses cannot accrue and be used or generated for that period. Loss utilization is effectively paused for that year.

The starting point for calculating the taxable income is to determine the taxable person’s accounting income as per their financial statements.

Generally, the formula is as follows:

Corporate tax return filing in UAE is completed online through the FTA’s system (EmaraTax platform).

Read more on how to calculate corporate tax.

For QFZP

Note

As a general rule, Financial Statements must be attached unless the taxpayer has elected for Small Business Relief.

Other supporting documents may need to be uploaded where relevant, while many working papers should be retained and provided if requested.

The corporate tax system in the UAE includes transfer pricing provisions that require related party transactions to adhere to the arm’s length principle.

The Tax Returns Guide outlines required components.

All submissions are made online through EmaraTax.

For businesses with multiple inadmissible or admissible expenses (i.e. fines and penalties), we recommend clients to segregate them in your Chart of Accounts.

The same goes with meals and entertainment for employees and customers or other counterparties. In short, we recommend for example having:

Keeping these expenses clearly separated at the accounting level makes corporate tax computations more accurate, reduces adjustment work at year-end, and helps ensure compliance.

Here are the penalties to expect in 2026, effective on 14 April:

| Premise | How much would it cost? |

|---|---|

| Late Registration Penalty | A fixed AED 10,000 penalty applies if you fail to register by the deadline set

Under First-period Penalty Waiver Snapshot, if the tax return (or annual declaration) for the first Tax Period is filed within 7 months from the end of that period, the late-registration penalty can be waived or refunded (even if already paid). Unfortunately, this is NOT a guarantee. |

| Late Filing of Tax Return | AED 1,000 for the first violation and AED 2,000 in case of repetition within 24 months. |

| Late Payment of Tax Due | If tax is payable but not settled by the deadline (9 months after the year-end), penalties may include a 14% per annum penalty charged monthly on unpaid amounts calculated from the day after the payment due date. |

| Failing to maintain or provide required accounting records and other information | AED 10,000 per violation, and AED 20,000 for repeat offenses within 24 months |

| Failure to submit requested information in Arabic | AED 5,000 per violation |

| Failure to inform Authority of amendments to tax record | AED 1,000 per violation; AED 5,000 if repeated within 24 months. |

| Late Deregistration

i.e. When a registrant fails to apply to de-register their business within 3 months from the date they cease to conduct business. For example, if the company has liquidated or permanently closed. |

AED 1,000 per month up to a maximum of AED 10,000 |

Penalties are administrative (monetary). Treat this as separate from any interest or additional charges the FTA may apply for overdue tax.

| Entity | Registration Deadline |

|---|---|

| Resident persons incorporated in the UAE | within 3 months from the date of incorporation in the UAE |

| Juridical persons incorporated outside the UAE, but effectively managed and controlled in the UAE | within 3 months from the end of the fiscal year in which the juridical person was registered under foreign jurisdiction laws effectively controlled by the UAE |

| Natural resident persons | before 31st March in the Gregorian calendar year after the calendar year in which the person exceeded AED 1 million in turnover |

| Entity | Registration Deadline |

|---|---|

| Permanent establishment (branches, subsidiaries, etc.) | within 6 months of its operations within UAE |

| Nexus in the UAE | within 3 months since establishment of the nexus |

| Natural person | within 3 months from the end of FY in which they become taxable in the UAE |

Failure to comply with tax regulations can lead to penalties for foreign firms operating in the UAE.

Businesses are required to retain records and supporting documents for at least 7 years following the end of each taxation period.

In addition, businesses must update their registration details within 20 business days when there are changes, such as:

Keeping business details official and accurate is core compliance requirement. This prevents administrative issues or potential risky penalties during audits and reviews.

The UAE corporate tax law requires businesses to register and file annual tax returns.

Despite clear rules, several recurring mistakes can expose businesses to adjustments, penalties or compliance risk.

Businesses operating in UAE may have a lot of nuance to navigate. An effectively managed taxation process helps to continuously monitor and smooth these things over.

Before corporate tax return filing, make sure to:

The UAE’s corporate tax regime aims to balance global tax standards with the country’s competitive business environment, which is beneficial for SMEs.

The corporate tax regime in the UAE is designed to support small and medium-sized enterprises (SMEs) by providing a lower tax rate on their initial income.

Proper record keeping can prevent a lot of headaches in the long run. Get in touch with our expert team to see how skrooge.ai can help you get your time back!

Businesses liable for Corporate Tax must file returns within 9 months of the end of the relevant Tax Period. Any tax payable arising from business profits tax must also be paid in the same timeline.

Audited financial statements are required only in specified cases, including Qualifying Free Zone Persons and Taxable Persons whose Revenue exceeds AED 50 million during the relevant Tax Period.

You can do this via FTA’s portal, EmaraTax.

Make sure to have the following prepared:

1. Financial Statements (including balance sheet, profit and loss statement, and other relevant financial information).

Audited Financial Statements are required only where applicable, including for QFZP and Taxable Persons whose revenue exceeds AED 50 million during the relevant Tax Period.

2. Corporate Tax Computation Working Papers

✔️ Reconciliation from Accounting Income to Taxable Income

✔️ Breakdown of tax adjustments

✔️ Schedule of Exempt Income

✔️ Add-back schedule for non-deductible expenses

✔️ Interest limitation computation

✔️ Any elections made (e.g., reliefs, accounting basis)

These working papers support the figures disclosed in the Tax Return.

3. Tax Loss Schedules (If Applicable)

✔️ Tax Losses brought forward

✔️ Tax Losses utilized during the current Taxable Period

✔️ Remaining carry-forward balances

✔️ Supporting documentation for loss origin

4. Related Party & Transfer Pricing Documentation (including intercompany agreements)

5. Free Zone Documentation (including proof of substance requirements)

6. Other Record keeping support

✔️ Accounting records

✔️ Invoices and contracts

✔️ Bank statements

✔️ Prior year tax returns

✔️ Corporate Tax Registration Number (TRN)

In practice, there is no standalone downloadable PDF or Excel template prescribed in the official UAE format. Everything is submitted through EmaraTax format.

However, we advise to keep a polished Chart of Accounts. Most businesses operating prepare an Excel internal working file to maintain paper trail on added tax and ensure accuracy before submission.

Once your tax returns are submitted, the system generates a PDF copy of the filed tax return that serves as the official filing record.

The FTA imposes penalties for late registration, delayed filing, inaccurate returns, and other violations.

You can check out our table on penalties to see the updated structure for 2026.

All Free Zone persons must register and file even at 0% tax owed.

Entities may be subject to Qualifying Free Zone status if:

✔️ They maintain adequate substance in the respective area

✔️ Derive income qualified at 0% tax rate

✔️ Comply with transfer pricing and arm’s length principle

✔️ Maintain audited statements

✔️ Meet the de minimis requirements for nonqualifying revenue

If the business elects to be taxed normally, the FZ entity becomes subject to standard CT rates and will be treated as any other taxable entity.

Thank you!

We've received your request and will get back to you shortly.

Loading...