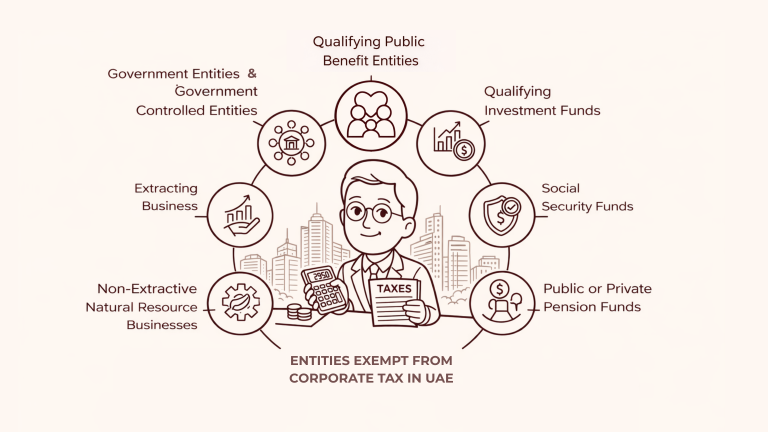

Transfer pricing UAE

What is transfer pricing in UAE? Transfer pricing is the set of prices applied in…

Not every accounting and bookkeeping firm is licensed to conduct a vast array of tasks. Some firms are focused purely on data entry, while others are authorized to provide tax advisory and audit services. Understanding the difference between each firm matters.

Picking the best accounting companies requires knowledge of VAT and corporate tax treatment in both mainland and free zones. The UAE government issued the Corporate Tax Law in December 2022, effective for financial years starting on or after 1 June 2023; VAT Law was introduced under Federal Decree-Law No. 8 of 2017 and came into effect 1 January 2018.

Both laws are still evolving to comply with the needs of the community and ensure competitiveness with the standards set globally. The UAE tax framework was updated earlier this year, with amendments being introduced by Federal Decree-Law No. 16 of 2025 affecting VAT Law, and Federal Decree-Law No. 17 of 2025 (Tax Procedures Law) bringing clarifications impacting Corporate Tax compliance.

Businesses need to understand all these changes to optimize financial and tax planning. Outsourcing accounting services offers scalability and flexibility, allowing businesses to adapt their financial support as they grow.

When accounting and compliance are handled by experienced accounting firms, founders regain time and strategic bandwidth to focus on product development, customer acquisition and market expansion.

As your business grows – whether through higher transaction volumes, market expansion or funding rounds – your financial reporting requirements evolve. A capable accounting firm adapts with you, offering tailored support as needed.

In this step-by-step guide, we provide you with a complete list of what to look for and how to gauge whether you are receiving real value for your investment.

With the implementation of the VAT Law, Corporate Tax Law and its amendments, entrepreneurs require more guidance navigating the complex regulations behind federal taxes.

Errors are no longer minor inconveniences as they trigger administrative penalties. Even worse, mistakes (however minor) represent risks by exposing entrepreneurs to administrative penalties and further audit by the federal government.

Beyond regulatory obligations, savvy business owners create their strategy based on financial visibility as it directly impacts how fast and confidently a business can grow.

Outsourcing financial tasks allows businesses to focus on core business priorities and strategic growth. A strong accounting firm in the UAE can build the financial infrastructure that allows businesses to:

In short, an on-point accounting firm in Dubai can become the strongest decision making support an entrepreneur needs at any stage in their business.

Note

Accounting firms in the UAE include the Big Four (KPMG, Deloitte, PwC, EY), mid-tier firms (Grant Thornton, BDO, etc.) and UAE/SME-focused players (like Skrooge). Big Four firms are known for their global reach and premium credibility, serving large multinational corporations, government entities, and publicly listed companies.

Many firms in the UAE support businesses with outsourced accounting and auditing services to ensure smoother operations.

Accounting firms in the UAE must navigate a complex regulatory environment including VAT (normally taxed at 5%) and Corporate Tax (standard rate at 9%). They also manage the company’s financial health by flagging receivables and payables, and ensuring that budgets are properly allocated and resources are properly managed.

Therefore, it is important that before comparing accounting firms, clarify your internal needs. Most mismatches happen because businesses outsource without defining scope. You can start by asking:

Certain firms offer a complete range of services such as bookkeeping, payroll, VAT advisory, internal/external audits, and CFO-level advisory. Many founders use these terms interchangeably. To illustrate, here’s the difference between each scope.

Service Type |

Definition of Scope |

What it means for your Business Setup |

|---|---|---|

Bookkeeping services |

Typically the most basic of functions when accounting firms are onboarded. |

|

Accounting services |

Preparation and analysis of financial statements to reflect the company’s financial position and performance. They are also in charge of preparing the data for financial reporting |

|

Tax services and support |

Advising on and managing compliance with UAE federal taxation laws, including VAT and Corporate Tax |

|

Audit services |

Often this is the type of Assurance Services used by businesses |

|

Advisory services |

Strategic financial guidance to support planning, forecasting, and long-term business decisions. Management consulting often falls in this category. |

|

This all starts with a good chart of accounts.

A Chart of Accounts (CoA) is the structured list of all the financial categories a business uses to record its transactions. In an accounting system (i.e. spreadsheet or software), the CoA is the menu of buckets where money gets sorted. It usually includes assets, liabilities, equity, revenue and expenses.

An average accountant works with the chart of accounts you provide. A great accountant starts by understanding your business model and designing your chart of accounts around that. This includes your unit economics, decision drivers, and your measures for success.

A good CoA is the data model of business decisions. If it is structure poorly, your reports can distort reality with flawed ROI analysis, misclassified costs and revenue leading to incorrect unit economics, and ultimately bad decisions on pricing, hiring and growth.

When the underlying structure is wrong, the numbers may appear precise when they are misleading. A great accountant understands that details matter and it starts with placing the correct structure to support.

Check out our Skrooge expert’s advice on maintaining your Chart of Accounts here.

When evaluating accounting and auditing firms in the UAE, it is good practice to go beyond brochures and ask for real evidence of capability.

The UAE Commercial Companies Law outlines how companies should be structured and remain compliant with local regulations.

Ask firms to demonstrate their real processes such as:

NOTE

UAE tax penalties are primarily imposed on the taxpayer, so your business remains responsible for timely and accurate filing and payment. If a firm acts as your registered Tax Agent, it has separate professional obligations, but this does not remove your company’s compliance risk.

Accounting and audit obligations differ between Free Zone and Mainland companies. Here are some of the differences and practical implications for reporting, audits, and tax compliance.

Considering that there are specific nuances to tax treatment for Mainland vs. Free Zone (including tax adjustments, loss carry forward, tax reliefs and other incentives available), it is best to consult a professional. Especially if this is your first time navigating the taxation landscape.

When talking about highly rated accounting firms in the UAE, confirm first that they have key credentials and are acknowledged by the authorities in place.

Professional qualifications matter particularly for audit, tax structuring, and financial management and advisory.

Depending on the services and set up being offered, verify that the firm is authorized to practice by having:

When evaluating highly rated accounting firms in the UAE, it helps to look at their credentials together with their firm’s Google or accredited platform for reviews (i.e. Glassdoor, Goodfirms, among others).

Having the right credentials matter for professional services. Here’s a list of professional qualifications you can check, especially for audit and tax advisory.

Outsourcing accounting services to a reputable firm in Dubai ensures that financial operations are managed by chartered accountants familiar with local requirements.

When evaluating their chosen accounting partner, most businesses focus only on immediate tax compliance needs. Based on our experience, it helps to avoid choosing narrowly and look into more long term needs.

For example, the average UAE business must operate with the following:

The right accounting partner should not just help you meet deadlines. They should help you interpret your numbers, structure your financial model intelligently, and make better strategic decisions as your business grows.

NOTE

Businesses in the UAE must comply with both local accounting regulations and international financial reporting standards (IFRS). The IFRS governs what is considered as generally accepted accounting principles and helpful for managing their accounting system set up.

When comparing advisory capabilities (especially for growth oriented companies), consider how the firms support your growth needs. A broader advisory service typically looks like:

Capability |

Typical “Compliance-Focused” Firm |

Advisory-Led Firm |

|---|---|---|

Bookkeeping |

✔ Transaction recording |

✔ + tailored Chart of Accounts Design |

Basic VAT filing |

✔ Standard filing |

✔ + VAT planning |

Corporate Tax returns |

✔ Filing support |

✔ + compliance and tax structuring strategy |

Free Zone advisory |

Limited |

Stays ahead for QFZP evaluation

|

Transfer Pricing |

Limited |

Structured documentation |

Cash flow forecasting |

Rare, usually works with data that’s already available |

Typically included in order to stay ahead of tax requirements |

Cost center analysis |

No |

Yes, in order to support your growth |

Management Reporting |

Basic reports |

CFO-level insights |

The FTA has actively encouraged digitalization efforts to make financial operations (FinOps) easier for business owners. With the launch of their integrated platform called EmaraTax, the FTA centralized access to FTA’s services and improved its tax administration. This shift is part of a broader expectation for businesses to maintain organized, digital and audit-ready records.

Many accounting firms in the UAE have since used modern accounting software to improve efficiency and accuracy. It also helps for business set up if you are familiar with what tools you need for your own operations. Some advisory firms charge fees on top (sometimes called hidden fees) so you can have your own access to this software. Top accounting firms, however bundle this up with their current services with more transparent pricing.

Accounting firms should use cloud-based accounting software for real-time financial dashboards and secure data management.

Examples of popular platforms include Xero, QuickBooks Online, and Zoho Books, all of which are widely known on a global scale by businesses regardless of their size.

When you set up your business in the UAE it is important to choose your accounting software at the outset of your business to avoid costly migration partnerships later on.

Some advisory firms charge additional fees for software access or limit your dashboard access. A transparent advisory firm will:

AI-enabled accounting technologies help automate:

Your chosen software is meant to decrease the risk of manual entry errors, late filings and delays in providing reports while maintaining a digital record of documents.

Note

The FTA maintains a public list of accredited eInvoicing system and software vendors. This is a useful reference when evaluating whether your accounting stack supports compliant digital tax workflows. Check it out here.

Top accounting firms in Dubai often use secured platforms to provide up-to-date tools for financial reporting.

When evaluating accounting and bookkeeping firms in UAE, ask:

Technology should enhance compliance.

Even the best accountants cannot compensate for poorly designed systems. Ideally, your cloud accounting tools should amplify:

You can read more about some of the best accounting software. We outlined best practices we have used in our 30+ years of experience.

When evaluating highly rated accounting firms in the UAE, communication and accountability matters just as much as technical skill.

A firm’s ability to respond promptly, provide structured reporting and guide you through fire fighting complex tasks (like transfer pricing documentation) can make the difference between staying ahead of issues and constantly putting out fires.

A Service Level Agreement (SLA) is a formal commitment from your accounting partner about how frequently you receive reports and how quickly they respond to queries. Clear SLAs help establish expectations and reduce misunderstandings.

For example:

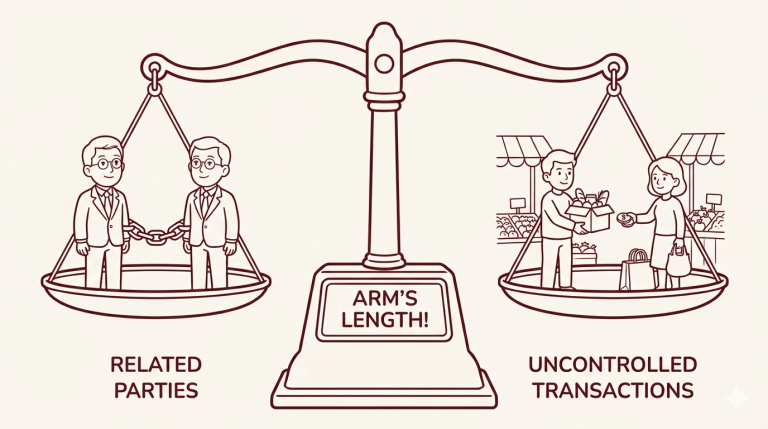

The Corporate Tax Law in the UAE includes formal transfer pricing rules for transactions with related parties, which must follow the arm’s length principle. This is codified in Article 34, which requires that dealings with related parties reflect terms that would occur between independent entities in similar circumstances.

The FTA also requires related-party disclosures in your tax return, and in many cases, formal documentation. UAE transfer pricing rules require related-party and connected person disclosures, and some businesses must also maintain formal transfer pricing documentation (including a Local File and, in some cases, a Master File) depending on the applicable thresholds and conditions.

Records must be kept for at least 5 years for VAT records and for corporate tax, records must be kept for at least 7 years after end of relevant tax period.

To illustrate the benefits and limitations of each model, here’s a quick table for reference:

Details for each Model |

Dedicated Manager |

Shared Pool Model |

|---|---|---|

Scope of Responsibility |

|

|

Pros |

|

Lower fees, broader resource pool |

Cons |

Often higher cost vs shared pool model |

Requires more coordination on your end, less continuity |

For businesses with intricate needs — such as transfer pricing documentation, cashflow forecasting, or strategic financial planning — a dedicated manager often delivers better long-term value. Sometimes, for higher volume clients, a dedicated team can be onboarded to handle different services of the firm.

Accounting services in the UAE generally follow the following pricing models:

Type of Billing |

Scope of Projects |

Cons |

|---|---|---|

Billed per hour of output |

You are charged based on time spent to deliver specific output.

|

|

Most common model for services in Dubai. You pay a fixed monthly fee for recurring services.

|

Without transparent pricing, these add-ons are where total cost often increases. |

|

Fixed service packages (often bespoke) |

Some firms offer bundled services under a structured package.

|

Transparency is what separates predictable pricing from surprise billings. It is hard to anticipate all potential scenarios for your business, so you will have to put faith that your package can cover a lot of ground. |

When comparing offers, make sure to clarify scope inclusions. Outsourcing services can reduce internal costs and help mitigate compliance risks, but transparent pricing ensures you avoid hidden costs. For example, Skrooge’s model is built around transparent, all-in monthly pricing for your peace of mind.

Browsing through a list of top accounting firms can be quite daunting. The industry comprises all kinds of practices, ranging from small practices to global audit and best accounting firms for large businesses.

The aim here is to identify the one that fits your needs, depending on your business stage, business structure, and tax complexity.

When creating a shortlist of firms in Dubai, use a structured screening process:

Not all accounting and auditing firms in UAE operate with the same level of discipline, internal controls or regulatory responsibilities. While pricing and branding matter, an errant employee can create long term risk for your business.

Below are warning signs to watch for when evaluation potential partners:

It helps if per stage, you look into:

The right firm should:

Outsourcing accounting allows entrepreneurs to focus on core competencies by reducing the time spent on financial tasks. Skrooge combines professional tax knowledge with AI-driven automation to provide organized accounting assistance.

Skrooge uses automation in accounting for routine work and professional acumen to assist businesses in minimizing time devoted to accounting while enhancing accounting compliance and strategic insight.

Accounting should not only be on time. It should also help businesses achieve your financial goals.

If you’re interested in knowing our services, feel free to drop your number and we will get right back to you.

Accounting firms in the UAE offer a wide range of services including bookkeeping, tax registration, and compliance. You can follow our step by step process in this article.

For bookkeeping, tax computations, and compliance support, firms may assist without being appointed as your Tax Agent, but formal FTA representation is a separate status.

There are many accounting firms in the UAE that offer registration, compliance, and tax services. Here is how you can check the legitimacy of the firm:

1. Check their Trade License from the concerned authority

2. Check FTA registration (in case of formal representation)

3. Check Auditor Registration (in case of conducting statutory audits)

In case the firm conducts statutory audits:

✔️ The auditor should be registered with the UAE Ministry of Economy.

✔️ The firm should have audit approval under UAE laws.

✔️ For Free Zone companies, the firm should be included in the list of Approved Auditors of that Free Zone.

✔️ In case the firm is not approved, their audit report will not be accepted by the concerned authority.

4. Check their professional credentials. You can ask for an ID card or membership verification from the firm. Although these credentials are not a substitute for registration, they assure technical skills.

Yes, in order for the audit report to be accepted by the relevant authorities, they must be registered on the Approved Auditors List.

Bookkeeping is the process of recording all financial transactions of a business. Accounting is the analysis of the financial data recorded in bookkeeping to gain insight into profitability, cashflows, cost of sales, financial sustainability, etc.

Big Four accounting firms and Dubai locals can handle both large corporations and SMEs if they perform their duties well.

There is no one-size-fits-all solution to this question. This is because it depends on your business size, complexity, and budget capabilities.

Large accounting firms are often a good fit for multinational groups, listed entities, and businesses with highly complex cross-border structures. Many SMEs and founder-led businesses, however, prefer reputable boutique firms for faster response times, more hands-on support, and more flexible pricing.

A Dubai local firm is ideal for SMEs since it is less expensive. However, a reputable firm can also be considered since it provides direct access to senior accountants.

This is because it provides faster response times, more practical and hands-on advice, and flexible pricing. This is often sufficient for SMEs operating in the UAE.

Thank you!

We've received your request and will get back to you shortly.

Loading...