How to choose your accounting firm in UAE: Tax, Audit and Bookkeeping services in Dubai

Not every accounting and bookkeeping firm is licensed to conduct a vast array of tasks.…

UAE’s corporate tax allows for businesses to be exempted from paying taxes. In this article, we explain exempted persons, tax rates, qualifying income for CT and eligibility criteria under the UAE Corporate Tax regime.

The UAE introduced a federal corporate tax regime effective for financial years beginning 1 June 2023. The objective of Federal Decree Law No. 47 of 2022 on the Taxation of Corporations and Businesses is to align with internationally recognized tax standards. The government aims to create a more competitive UAE economy with diversified government revenue sources.

Under Federal Decree-Law No. 47 of 2022, Corporate Tax is generally charged at 9%, with a 0% rate applying to the portion of Taxable Income up to the threshold amount set by Cabinet decision (currently AED 375,000).

A separate QFZP rate framework of 0% on Qualifying Income and 9% on Taxable Income that is not Qualifying Income (subject to conditions). This is separate from the concept of an “Exempt Person” under Article 4.

Corporate Tax applies for taxable income (derived using business profits adjusted) earned by taxable persons in a tax period, calculated on a self-assessment basis.

The Federal Tax Authority (FTA) is in charge of administering tax obligations through their official EmaraTax portal, with policies and legislation under the scope of the Ministry of Finance.

For clarity, exemption of persons is different from 0% tax rate or Small Business Relief, as the latter are considered as tax treatments on income and not exemption from the law itself.

Resident UAE businesses are also given taxation reliefs through the introduction of Small Business Relief (SBR) and tax loss carry forward. As of the date of writing, Small Business Relief (SBR) applies only where the relevant and previous Tax Period revenues stay within the AED 3 million threshold, and the relief is time-limited to Tax Periods ending on or before 31 December 2026 (unless the rules are changed).

For the purpose of this article, we will discuss who is exempted from UAE CT regime and their eligibility, registration processes, and practical tips for entrepreneurs navigating federal corporate tax.

Note

Businesses can apply for Small Business Relief if their revenue is below AED 3 million in relevant tax periods, allowing them to be treated as having zero taxable income until December 31, 2026.

Under Article 4 of Federal Decree Law No. 47, corporate tax exemption happens when a person or entity is legally excluded from paying corporate tax, either because the entity is completely exempt or is exempt on specific types of income under the UAE CT law.

This is different from (i) a 0% Corporate Tax rate, and (ii) Exempt Income rules that may apply to specific income streams when calculating Taxable Income. In other words, an entity can be within the Corporate Tax regime and still have a 0% rate or Exempt Income treatment without being an Article 4 Exempt Person.

Exemption can be automatic (i.e. granted directly by the law) or conditional – requiring application, approval and ongoing compliance.

Note:

Being exempted does not always remove registration or filing obligations. Some companies are still subject to:

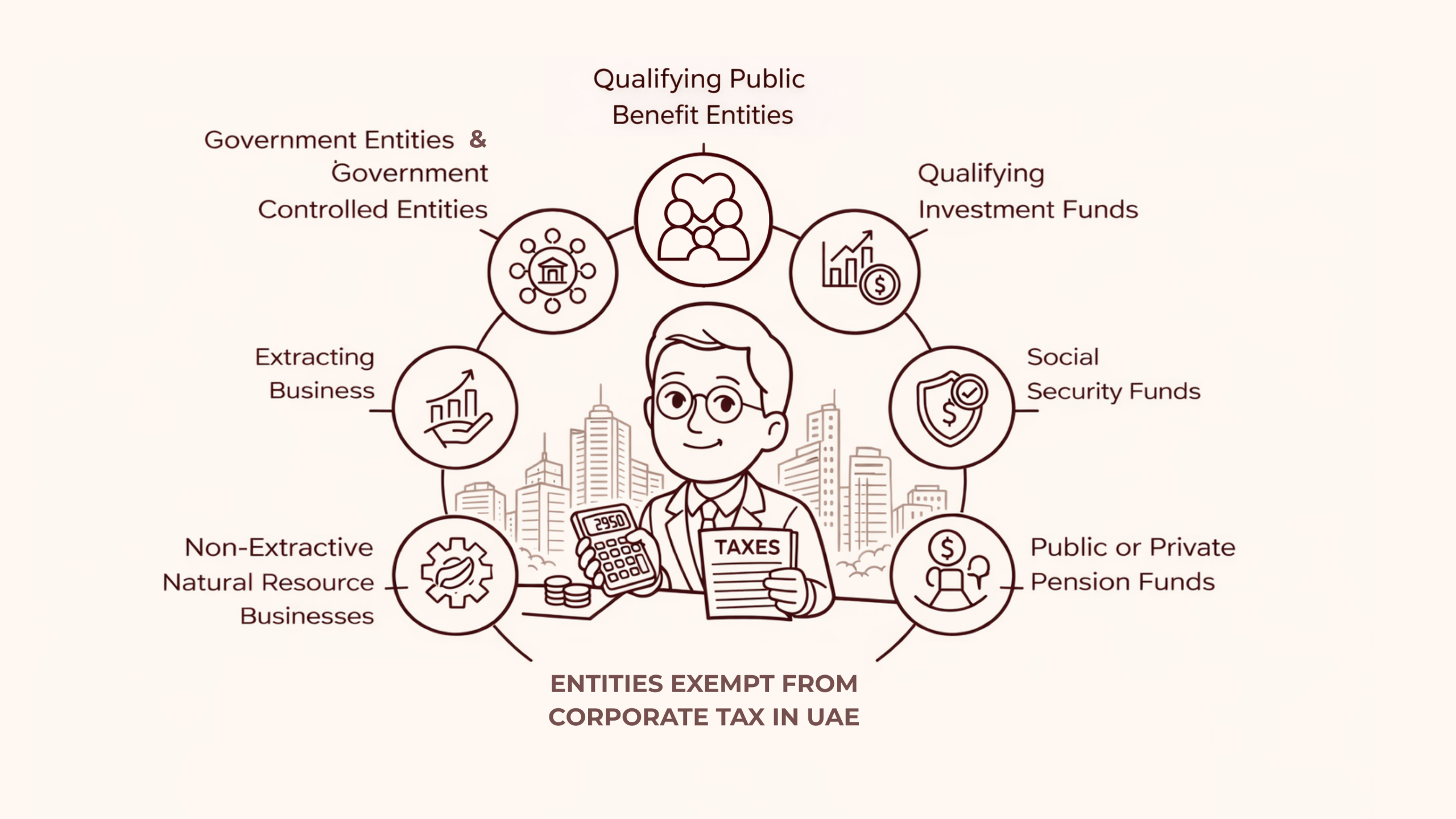

An entity qualifies for exemption only if it falls within the categories explicitly recognized by the UAE Corporate tax Law and meets relevant conditions. Exempt Persons are a separate legal category under the Corporate Tax Law and are not subject to Corporate Tax while their exemption conditions continue to be met.

Exemption is not based solely on size or industry alone. The United Arab Emirates classifies based on legal status, purpose of the business operating and corresponding regulatory supervision.

Government entities are automatically exempt by law, as long as they only carry out their mandated activities. Under the Corporate tax law, this includes federal government entities, Emirate-level government entities, ministries and institutions established by the state and other government departments and authorities.

Government controlled entities are exempt without needing to apply unless they conduct licensed commercial activities. Once they engage outside their mandated activities, the exemption may not apply and the operations under a license may fall within the scope of Corporate Tax.

To be eligible, government controlled entities must be 1) wholly owned and controlled by a government entity, and 2) established to carry out a public interest or governmental function.

These are activities that fall within:

An extractive business refers to the extraction of natural resources (such as oil, gas, minerals, and similar non regenerating resources). Typically, these activities are carried out under a concession, license, or agreement granted by the local government.

Certain non-extractive natural resource businesses refer to businesses operating on activities related to natural resources that are not directly engaged in extraction. These businesses must operate under a license or agreement from the local government.

The tax treatment for both an extractive business and certain non-extractive natural resource businesses is considered exempt and remain subject to Emirate-level taxation.

For example, an oil extraction company operating under a government concession is exempt. However, if the same company decides to run a commercial trading business outside of their license, then this becomes subject to corporate tax.

Note

In summary, for extractive businesses and non-extractive natural resource businesses to qualify for exemption, they must:

If the same entity conducts other commercial business activities that are not covered by the license, then these activities fall within the scope of paying corporate tax.

A Qualifying Public Benefit Entity is conditionally exempt entities, subject to approval. Exemption is not automatic and requires formal recognition.

Examples of public benefit organizations include:

To qualify for exemption, the entity must meet the conditions under Article 9 of Federal Decree-Law No. 47 of 2022:

To encourage investments for economic growth, investment funds can seek tax relief from the UAE corporate tax if they meet certain conditions specified by the law.

Under Article 10, this exemption is also conditional and does not apply automatically.

A Qualifying Investment Fund is an investment vehicle and exempted when it:

Exempt status applies prospectively from the approved Tax Period.

The law itself does not define one single authority. Instead, “competent authority” refers to the relevant UAE regulator that has legal jurisdiction over the fund.

In practice, jurisdiction can fall under any of the following:

However, the Corporate Tax Law uses the general blanket term of competent authority because it depends on where the fund is established, and under which regulatory framework it operates.

Note

A Recognized Stock Exchange under the corporate tax law is a licensed and regulated exchange in the UAE or abroad (subject to Ministerial conditions). While it is not an exempt person, it is relevant in determining whether dividends and capital gains from listed shareholdings qualify for participation exemption.

Listing on a recognized stock exchange can affect and help a shareholding qualify for participation exemption treatment.

Public and Private Pension and Social Security Funds in the UAE are established to provide financial security and income support to citizens in cases of retirement, disability, death and/or end of service.

These funds operate as part of the governments broader social protection system and safeguard contributors through regulated contribution systems.

In the government sector, these funds are managed by dedicated federal and local authorities, and apply primarily to UAE nationals working in federal and local government entities, and certain private sector organizations where applicable under law.

The system is contribution based, wherein employers and employees contribute a percentage of salary. Benefits are calculated based on contribution or service duration and salary structure.

Due to its nature, these are considered as exempt from paying corporate tax. Exemption applies only while the fund maintains its regulated status and meets additional conditions prescribed by the Ministry of Finance.

Any wholly owned and controlled subsidiaries by exempted entities may be subject to exemption if conditions are met.

Eligibility Conditions |

A subsidiary may qualify if:

|

Permitted Activities |

The subsidiary must limit its activities to:

|

Restrictions |

Subsidiary must not engage in unrelated or standalone commercial business activities. Additionally, it must continue meeting ownership and control requirements with the parent companies. |

The UAE government has introduced various exemptions on income to support free zones and other independent businesses.

The government preserves Free Zone incentives through a specific framework designating Qualifying Free Zone Person (QFZP) status if eligible. However, not all businesses operating in the free zone are eligible for exemption from corporate tax.

UAE’s Free Zone businesses must meet adequate economic substance requirements to qualify. The entity must carry out its core income-generating activities (CIGA) within the Free Zone and maintain appropriate staff, premises, and operational resources relative to its activities.

You can read more about the requirements for status eligibility in our article on Filing for Corporate Tax for QFZPs.

A QFZP benefits from 0% corporate tax on qualifying income and 9% on nonqualifying income.

To qualify and maintain QFZP status, a business must be:

If the entity fails to meet the conditions, QFZP status is lost from the beginning of the Tax Period and the loss extends to the following four Tax Periods. During this time, the entity becomes subject to standard corporate tax rules during this period.

The QFZP framework separates qualifying and nonqualifying income to preserve incentives without distorting the mainland economy. General rule is qualifying revenue comes from permitted activities and transactions; nonqualifying income is taxed to ensure that preferential treatment is tied to genuine economic activity.

Classification depends on the type of activity, status of the entity and sources of income.

As a rule, qualifying income (0% on income eligible for exemption) generally includes:

A QFZP’s Taxable Income that is not Qualifying Income is taxed at 9%. This can include income from Excluded Activities and other income that falls outside the QFZP qualifying rules.

Important:

Mainland (non-Free Zone) income is not automatically non-qualifying. The treatment depends on the activity type, whether it is an Excluded Activity, and whether the QFZP conditions are satisfied.

Businesses are not “exempt” merely because their Taxable Income is below AED 375,000. Instead, a 0% Corporate Tax rate applies to the portion of Taxable Income up to the threshold, and the standard 9% rate applies to the excess.

This threshold aims to support small and early stage businesses while maintaining a standard corporate tax structure.

The threshold applies to taxable income, not revenue.

To arrive at the income subject to tax, take your accounting profit and + tax adjustments, including nondeductible expenses, relevant income exempted from tax, and any other reliefs by law.

The threshold does not create an “exempt person” status, and is separate from Small Business Relief, which is based on a revenue threshold (AED 3 million) and is time limited to 31 December 2026 as of publishing date.

The threshold does not remove registration or filing obligations.

Corporate Tax registration is handled through the FTA (via EmaraTax), but not all exempt categories follow the same registration or application path.

Some Exempt Persons are not required to register for Corporate Tax, while other exempt categories must register and may also need to submit an exemption application/approval package.

If exemption conditions are breached or such businesses carry out activities outside the permitted scope, the entity ceases to be exempt from the start of the Taxation Period.

The entity is now treated as a single taxable person. The loss of exemption applies from the start of the tax period in which conditions were not met.

Limited exceptions apply if in certain cases, the failure to meet conditions is “temporary” and corrective measures are promptly taken. However, this is not automatically the case and continued monitoring is advised to retain exempt status.

Here are some other tips and examples we see in founder-led businesses when setting up their UAE Corporate Tax compliance.

Tips |

Why this Matters |

How we can support at Skrooge |

|---|---|---|

Register early and correctly — even if you expect an exemption |

Registration depends on your status. All Taxable Persons must register for Corporate Tax, while Exempt Persons follow category-specific registration rules |

Skrooge supports corporate tax registration classification. We help founders avoid incorrect assumptions at setup and reduce future work. |

Don’t confuse the requirements for corporate tax exemption, 0% tax rate and income reliefs. |

Exemption, 0% rates, and Small Business Relief are different concepts with different compliance rules. |

Skrooge’s accountants help founders interpret the correct tax status, rather than relying on license type or hearsay. |

Track qualifying vs non qualifying income from day one |

This is critical for Free Zone entities looking to qualify for QFZP status. |

Skrooge uses our AI-powered automated transaction tagging and accountant’s review to ensure income is classified correctly for Corporate Tax purposes. |

Maintain clean books and accounting records |

Financial statements & proof of corporate tax exemption rely on documented evidence. |

Skrooge handles monthly bookkeeping, reconciliations, and document collection so records are always audit-ready. |

Watch deadlines and changes in conditions closely |

Exempt or preferential status can be lost if conditions are no longer met. |

To avoid being treated as other businesses subject to corporate tax, skrooge.ai highlights expiry dates and compliance deadlines with proactive reminders. |

Avoid “set and forget” operational structures. |

Changes in ownership, activities, or group structure can affect UAE’s corporate tax exemption eligibility and must be reflected promptly. |

Skrooge provides ongoing tax advisory, flagging risks before they become filing or penalty issues. |

Use tools to speed things up, but keep final judgment with expert people you can trust |

Automation reduces errors and speeds up reporting, but navigating the Corporate Tax regime requires nuance and interpretation. |

Skrooge deliberately combines AI for routine work with accountant judgment to identify edge cases, so founders get speed and accountability. |

The corporate tax regime is intended to empower the national economy and help the UAE achieve its strategic objectives.

Recently, the Cabinet Decision No. 129 of 2025, effective April 14, 2026, revises the UAE’s administrative penalty framework for tax violations. In this article, we highlight the updated penalty system for 2026.

To learn more about our services specific to corporate tax, visit our homepage. You can also check your pricing based on monthly transactions.

Have other questions? Leave us your number and we will call you right back.

A business qualifies for exemption if they are either an exempt person outside the scope of corporate tax or earning income eligible under UAE corporate tax exemption.

The following apply under exempt persons, subject to conditions:

✔️ Government entities and Government Controlled Entities

✔️ Certain Non-extractive natural resource business and extractive natural resource businesses

✔️ Eligible Qualifying Public Benefit Entities

✔️ Qualifying Investment Funds

✔️ Private and public pension & Social Protection Funds

✔️ Wholly Owned UAE Subsidiaries of Persons Exempted under UAE Tax Law

For non-extractive businesses, once they divert into commercial activities, then those activities become treated with corporate tax.

Similarly, the following may be excluded and not subject to corporate tax during tax income calculation

✔️ Qualifying participation dividends

✔️ Certain foreign permanent establishment income (if elected)

✔️ Income of qualifying public benefit entities (if approved)

All Taxable Persons in the UAE must register with the FTA for Corporate Tax. Exempt Persons follow separate rules, and some exempt categories are not required to register.

Qualifying vs nonqualifying income allows Free Zone businesses under QFZP status to operate within the Free Zone and Mainland.

As a rule, qualifying revenue (0% tax rate on income eligible for exemption) generally includes:

1. Income from transactions and business activities with other free zone persons

2. Income from permitted qualifying activities as per applicable CT regulation

3. Income that is not derived from explicitly stated excluded activities.

Nonqualifying income (9% is taxed on other revenue) generally includes:

1. Income that is not derived from Qualifying Activities (or that falls under Excluded Activities).

2.. Income from excluded activities

3. Certain UAE sourced income that does not meet qualifying conditions

To keep their 0% tax rate benefits, such businesses must satisfy the de minimis threshold for nonqualifying income (i.e. non-qualifying revenue must not go beyond AED 5 million or 5% of total revenue, whichever is lower), provided that all other eligibility requirements are met.

Corporate tax applies to Free Zone businesses in the UAE, but eligible entities may benefit from a 0% rate if they meet the conditions to be treated as a Qualifying Free Zone Person.

For partially exempt businesses, CT is calculated only on the portion of income that is not exempt.

Step 1: Start with net profits as reflected in its financial statements

Step 2: Identify income that qualifies as exempt (e.g. qualifying revenue earned)

Step 3: Determine taxable income by making tax adjustments to the remaining portion of net profits (adjusted to nondeductible expenses)

Step 4: Apply the applicable tax rate using the AED 375,000 threshold or under QFZP status.

For non-residents, the analysis usually turns on whether they have a UAE Permanent Establishment, UAE nexus, or taxable UAE-sourced income under the Corporate Tax Law.

Separately, the Corporate Tax Law provides for a 0% withholding tax rate on relevant State-Sourced Income categories (unless a different rate is specified by Cabinet decision).

Submit the following documentation to the FTA to prove eligibility:

✔️ Legal structure and details on the nature of activities

✔️ Ownership structure and control

✔️ Regulatory oversight from applicable legislation

✔️ Document supporting the entity is listed in a Cabinet Decision in cases required.

If exemption conditions are breached or carry out activities outside the permitted scope, the entity ceases to be exempt from the start of the Taxation Period.

The entity is now treated as a taxable person. The loss of exemption applies from the start of the tax period in which conditions were not met.

Corporate tax is a direct tax levied under a tiered tax bracket system wherein:

Taxable income up to AED 375,000 -> 0% corporate tax rate

Taxable income > AED 375,000 -> 9% rate on the excess

This article provides general information on UAE Corporate Tax and does not constitute tax advice under applicable laws. Corporate Tax treatment may vary depending on individual circumstances. Readers should seek professional advice before making any decisions.

Thank you!

We've received your request and will get back to you shortly.

Loading...