How to choose your accounting firm in UAE: Tax, Audit and Bookkeeping services in Dubai

Not every accounting and bookkeeping firm is licensed to conduct a vast array of tasks.…

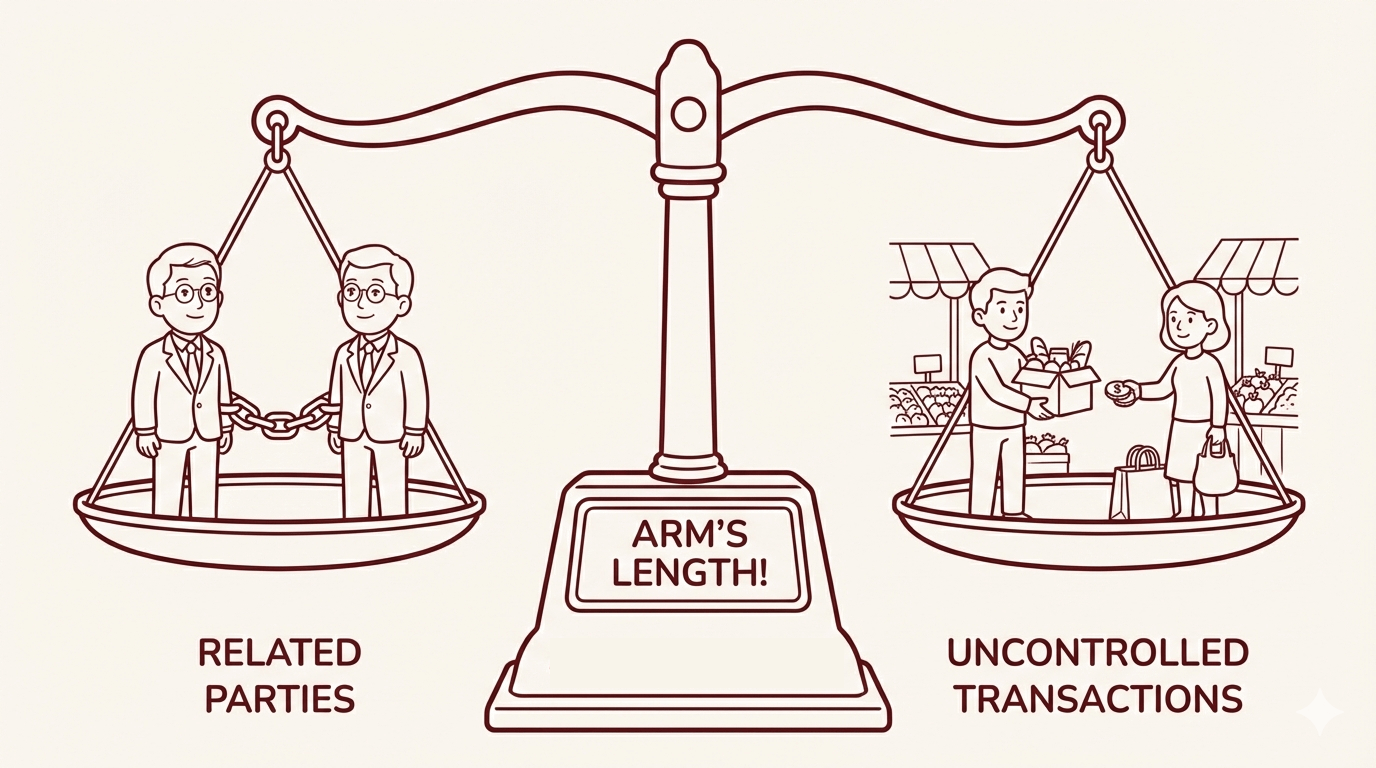

Transfer pricing is the set of prices applied in transactions between related parties, such as parent companies, subsidiaries, key management personnel, and key shareholders. Transfer pricing in the UAE must meet the arm’s length principle, i.e., all related party transactions must be recorded as if the two parties were unrelated and entering into a similar transaction under similar circumstances. This principle ensures that tax is charged where value is created and not in a manner that artificially minimizes the tax bills for businesses. Under the UAE Corporate Tax regime, businesses must also consider Connected Persons rules (for example, certain payments to directors, related persons, etc.), which are addressed separately under the law.

When the UAE Ministry of Finance (MoF) introduced corporate tax through the Federal Decree-Law No. 47 of 2022, it defined the UAE’s transfer pricing regulations in line with OECD Transfer Pricing Guidelines of 2022.

To comply with the UAE Corporate Tax Law, UAE businesses must apply one or a combination of the following transfer pricing methods to show that they have complied with the arm’s length principle:

A common element among these methods, or rather under the UAE’s transfer pricing guidelines, is that transactions are classified as controlled if they involve two related parties and uncontrolled if the two parties are unrelated. So, to oversimplify, businesses must essentially prove that their controlled transactions are not materially different than any similar uncontrolled transactions.

Typically, an uncontrolled transaction qualifies as a comparable transaction when there are significant similarities in the timing, contractual terms, and type of goods/services being transacted.

Once you establish the arm’s length price using one of the listed methods, you must simply compare it with the controlled transaction price to see if you met the transfer pricing requirements.

The Comparable Uncontrolled Price (CUP) method compares the price charged in a controlled transaction with the arm’s length price (market price) in a comparable uncontrolled transaction.

If there are no differences between a controlled and an uncontrolled transaction that could materially impact the price in the open market, you can take the uncontrolled transaction’s price as the arm’s length price. If any material differences exist, you must make the appropriate adjustments to arrive at the arm’s length price.

Under the UAE Corporate Tax framework, businesses should apply the most reliable transfer pricing method for the facts and circumstances of the transaction. In practice, the CUP method is often preferred where reliable comparison base is available, but method selection should be supported by a comparability analysis.

The resale price method is applied to transactions involving goods transferred from one related party to another for resale to unrelated parties. In this method, you must apply an appropriate resale price margin to the selling price in the unrelated party transaction to arrive at the arm’s length price.

Typically, the appropriate resale price margin would be the margin in a similar resale where the goods were procured from an unrelated party, and the reseller did not add any significant value to said goods.

So, if the reseller has a powerful brand or processes the goods materially, the resale price method cannot be used.

When you apply the RPM, similarities between the operations of the related party supplier and the independent supplier are an important requirement for comparability.

Also, since the accounting treatment may differ for related party transactions and transactions with independent entities, you must adjust the resale price margin accordingly.

The cost-plus method is similar to RPM. It involves applying a reasonable mark-up to the cost of goods and services received from related parties to establish the arm’s length price. When you calculate the reasonable mark-up, just like RPM, you will need to account for differences in accounting policies. The key difference is that this method takes the functions performed by the seller into account and can be applied to goods as well as services.

So, CPM is appropriate when semi-finished goods are sold between related parties, they have entered long-term supply agreements (LTSAs), and when the transaction involves the supply of services.

The transactional net margin method is similar to CPM and RPM since it involves establishing an appropriate net profit margin for controlled transactions based on the net profit margin in comparable independent party transactions.

Here, you need to establish comparability between your business and a third party so you can use its net profit margin as the arm’s length margin, directly or after appropriate adjustments.

Comparability is established between your business and the third-party have similarities regarding relevant factors such as capacity utilization, business strategies, management efficiency, cost structure, market structure, cost of capital, business experience, and accounting treatments of the relevant expenses.

If any material difference in such operating circumstances exists, the arm’s length net margin must be established by making appropriate adjustments to the third-party transaction’s net profit margin.

Since any differences in the functions performed between two transactions will directly reflect in the operating expenses, TNMM offers more flexibility in what qualifies as a comparable transaction. In comparison, the CUP method, RPM, and CPM do not consider operating expenses.

The transaction profit split method, or simply the profit split method (PSM), involves calculating the combined profits of related parties and then splitting them across entities as per the arm’s length principle. In practice, the PSM is often considered where related parties are highly integrated, make unique and valuable contributions, or share economically significant risks, subject to a proper comparability and functional analysis.

When you are determining the appropriate profit split, you must consider each entity’s contributions, functions performed, assets used, and risks assumed. These inputs must be measurable and consistent with the functional analysis of controlled transactions under review.

If there’s no comparable data involving independent parties, you can either use the contribution analysis approach or the residual analysis approach for establishing the profit split. As the name suggests, the contribution analysis approach involves allocating profits across related parties based on their contributions.

In the residual analysis, you must first allocate an arm’s length return for each routine function based on any of the listed transfer pricing methods. Then, any residual profits in excess of the combined arm’s length returns are allocated as per the contribution analysis approach or any other appropriate method that takes the circumstances of the transaction into account.

Note

UAE Transfer Pricing Guidelines allow you to choose a transfer pricing method other than the ones listed in Article 34 of Federal Decree Law No. 47 of 2022 if you can prove that none of these methods can reasonably capture the circumstances of a related party transaction, as long as the alternative method satisfies the arm’s length principle.

UAE’s transfer pricing guidelines apply to Taxable Persons that enter into transactions or arrangements with Related Parties, and to relevant dealings with Connected Persons under the Corporate Tax Law. If you engage in transactions with your related parties, the transactions must mandatorily be recorded at arm’s length. If the tax authorities find any violations of this rule, they will adjust your taxable income and update your tax return. Companies that have raised funds by issuing shares and/or bonds also need to demonstrate that their key management personnel’s compensation and dealings with any other connected persons were executed at arm’s length to appease their investors.

The Transfer Pricing Disclosure schedules in the UAE Corporate Tax return are completed based on FTA thresholds. In general, the Related Party Transactions Schedule is triggered where the total value of all Related Party transactions in the Tax Period exceeds AED 40 million, and category-level details are then reported where the total value in a category exceeds AED 4 million. The Connected Person Schedule is generally triggered where the total value of transactions with a Connected Person exceeds AED 500,000 in the Tax Period.

It is important that the information provided in the transfer pricing disclosure form is consistent with your corporate tax return to avoid queries or adjustments from the tax authorities.

The disclosures in this form can be summarized as:

Related party transaction category whose value exceeds AED 4 million |

Connected persons with whom transactions total AED 500,000 |

|---|---|

|

|

UAE transfer pricing documentation thresholds distinguish between Master File and Local File requirements.

A Master File and Local File are generally required where the Taxable Person is part of an MNE Group and the group’s consolidated revenue exceeds AED 3.15 billion in the relevant Tax Period.

A Local File is also required where the Taxable Person’s own revenue exceeds AED 200 million in the relevant Tax Period (even if the MNE threshold is not met).

In the transfer pricing master file, you must provide a comprehensive overview of the multinational group’s global operations, including its organizational structure, businesses, intangible assets, intercompany financial transactions, and its financial and tax positions.

Reporting category |

Description |

|---|---|

Organizational structure |

A chart of your group’s legal and ownership structure, which also details the location of each entity |

Description of your group’s businesses |

|

Intangible assets |

|

Intercompany financial activity |

|

Group’s financial and tax positions |

|

Then, in the local file, you must provide the local entity’s financial information, an analysis of each material category of related party transaction, a description of the transfer pricing method, and other relevant information.

In the local file, certain related party transactions must compulsorily be documented, and some are exempt from documentation. Here’s a comprehensive list:

Transactions that must be documented in the local file |

Transactions exempt from documentation in the local file |

|---|---|

Related party transactions involving:

|

Related party transactions involving:

|

Caution!

Regardless of whether a related party transaction is not compulsorily documented or exempt from documentation, it must still be recorded as per the transfer pricing guidelines.

Your business crosses the UAE transfer pricing threshold for maintaining a master file and a local file if:

Transfer pricing impact assessment in the UAE context helps understand a business’s exposure to restatements and corporate tax penalties. It involves reviewing business relationships and transactions with related parties and then assessing existing documentation, such as disclosure forms, master file, and local file.

This exercise will help you understand any gaps in your RPT-related bookkeeping.

While it is possible to conduct this exercise with in-house personnel, hiring third-party experts like Skrooge is a best practice. External auditors will bring knowledge of the UAE corporate tax law nuances and a fresh perspective free of biases.

Whichever transfer pricing method you use, whether it is one of the five prescribed methods or any other method, a key input is comparable uncontrolled (non-RPT) transactions. A benchmarking study is the process of identifying comparable uncontrolled transactions.

Comparable uncontrolled transactions can either be internal or external. Internal uncontrolled transactions are transactions between your group members and one unrelated party, while external uncontrolled transactions are between two entities unrelated to each other and the group.

If the functions carried out by group members are also sometimes outsourced to independent entities, you will have a library of internal comparable uncontrolled transactions.

However, many groups do not have such a library since the focus is on internalizing costs by relying mainly on related parties.

In such cases, you will need to perform a benchmarking study using external comparables, such as publicly quoted prices (where an active market exists) and commercial databases, and then make appropriate comparability adjustments where needed.

You must bear in mind that uncontrolled transactions qualify as comparable when there are significant similarities, such as timing, type of good, quantity, and contractual terms. The contractual terms of RPTs are often laid out in long-term supply agreements (LTSAs). In contrast, it is rare for unrelated parties to enter into LTSAs. Fortunately, the UAE corporate tax law allows you to adjust uncontrolled transactions to enhance their comparability.

This UAE corporate tax transfer pricing guide covers one of the most overlooked compliance areas for businesses filing their first corporate tax returns, i.e., the direct link between related party transactions, taxable profits, and your CT liability.

Transfer pricing directly impacts the taxable profits reported in the corporate tax return of all related parties. So, you must ensure that your transfer pricing disclosure form is consistent with the corporate tax returns to avoid scrutiny from regulators.

Transfer prices also help evaluate the profitability and efficiency of individual business units, providing valuable insights for management and compliance.

Key takeaway

Transfer pricing is not a standalone exercise. It must be integrated into your CT return preparation process from the start of the tax period, not treated as an afterthought once the books are closed.

If the prices charged in related party transactions deviate from those that would be charged between unrelated parties, the FTA has the authority to adjust the taxpayer’s taxable income to reflect the arm’s length price.

To reduce the risk of transfer pricing adjustments and to support your tax position, you should prepare and maintain transfer pricing documentation and ensure your pricing is arm’s length in substance, not just on paper.

The transfer pricing adjustment works in both directions. Suppose a UAE entity is overcharged by a related party, say through inflated management fees or above-market intercompany loan interest. Then, its deductible expenses will be reduced to arm’s length levels. At the same time, the related party’s revenue will be adjusted to reflect the arm’s length price.

Double taxation is a potential risk in transfer pricing when the same income is taxed by more than one jurisdiction. This can occur if the Federal Tax Authority (FTA) in the UAE makes a transfer pricing adjustment that increases a taxpayer’s taxable income, while a foreign tax authority also taxes the same income in its jurisdiction. Such situations can lead to increased tax liabilities and financial strain for businesses operating across borders.

To address this risk, the UAE has implemented several relief mechanisms. The mutual agreement procedure (MAP) allows taxpayers to seek resolution when double taxation arises from transfer pricing adjustments, enabling the UAE and the other involved country to negotiate a fair outcome. Additionally, advance pricing agreements (APAs) provide certainty by pre-approving transfer pricing arrangements.

The UAE has an extensive treaty network that can be relevant when seeking relief from double taxation in cross-border transfer pricing cases. You could check the latest Ministry of Finance treaties dashboard at official website.

Advance Pricing Agreements (APAs) are available in the UAE as a proactive tool for managing transfer pricing risk. An APA is a formal agreement between a taxpayer and the Federal Tax Authority (FTA) that establishes the transfer pricing methodology to be applied to specific transactions over a set period. By entering into an APA, businesses gain certainty that their transfer pricing arrangements will be accepted by the FTA, reducing the risk of future disputes and adjustments.

The UAE’s APA program is designed in line with the OECD Guidelines, and currently allows for domestic unilateral APAs. In 2026, the FTA is expected to roll out cross-border APAs. The tax authority also plans to later introduce bilateral and multilateral APAs.

The APA application process can be summarized as follows:

| APA application | APA renewal |

|---|---|

| AED 30,000 | AED 15,000 |

Transfer pricing regulations in the UAE are still relatively new, and businesses are making avoidable errors that create significant audit risk.

The most frequent transfer pricing compliance issues we encounter include:

Under UAE corporate tax law, failure to maintain adequate transfer pricing documentation or to apply the arm’s length principle can result in taxable income adjustments and administrative penalties under the UAE tax framework.

To remain audit-ready, you should ensure your disclosure forms, master file, and local file are completed accurately and on time, your benchmarking studies are refreshed periodically, and your intercompany agreements are documented in writing and reflect actual conduct. If the FTA requests transfer pricing documentation, the Corporate Tax Law generally requires it to be submitted within 30 days (or a different period if specified by the FTA). Transfer pricing disputes may arise with tax administrations regarding adjustments or compliance, but these can be resolved through available dispute resolution mechanisms.

Here are some of the best practices for arm’s length principle compliance in the UAE:

Navigating UAE transfer pricing rules requires legal, financial, and industry-specific expertise that most businesses cannot maintain entirely in-house. Transfer pricing services in the UAE cover the full spectrum of compliance needs, from benchmarking studies and documentation to audit defense and advance pricing agreements.

Transfer pricing advisory in the UAE generally includes the following:

Internal teams often lack access to benchmarking databases, and their familiarity with existing arrangements can introduce blind spots when assessing compliance risk. UAE transfer pricing services from external advisors like Skrooge bring objectivity and an up-to-date knowledge of how the FTA interprets the arm’s length principle in practice.

UAE transfer pricing regulations require you to record related party transactions as per the arm’s length principle so that corporate tax is charged where value is created instead of allowing for tax evasion by misallocating profits.

Transfer pricing impact assessment involves mapping related party transactions and reviewing existing transfer pricing methods and documentation to understand your exposure to taxable income adjustments and penalties.

In the UAE Corporate Tax return, the Transfer Pricing disclosure schedules are triggered based on FTA thresholds. Broadly:

• Related Party Transactions Schedule is triggered when total Related Party transactions exceed AED 40 million in the Tax Period, with category-level reporting where a category exceeds AED 4 million; and

• Connected Person Schedule is triggered where total transactions with a Connected Person exceed AED 500,000 in the Tax Period.

Separate thresholds apply for maintaining a Master File and Local File.

The most common triggers include failing to maintain any documentation for related party transactions, applying an inappropriate transfer pricing method, omitting connected persons from the disclosure form, treating intercompany loans informally without market-rate interest or written agreements, and using outdated benchmarking studies that no longer reflect current business circumstances.

Under UAE corporate tax law, businesses are required to retain records and documents for a minimum of seven years from the end of the relevant tax period. This includes all TP documentation, such as benchmarking studies, master files, local files, intercompany agreements, and disclosure forms.

No. UAE transfer pricing rules apply to all businesses subject to corporate tax that transact with related parties, regardless of size.

Thank you!

We've received your request and will get back to you shortly.

Loading...